Ecommerce bookkeeping involves tracking and managing the financial transactions of online businesses, from sales revenue to operating expenses. In the fast-paced and competitive world of ecommerce, accurate bookkeeping isn’t just an administrative task — it’s the backbone of informed decision-making and growth. Effective bookkeeping helps ecommerce business owners understand their financial health, optimize spending, prepare for tax season, and plan for future growth.

Whether you’re a small online retailer or a large ecommerce brand, proper bookkeeping practices are essential for navigating the complexities of digital business. MonkTaxSolutions specializes in helping ecommerce businesses streamline their financial processes, ensuring accuracy and compliance with U.S. regulations. This guide explores the essentials of ecommerce bookkeeping, focusing on best practices, tools, and strategies tailored for businesses in the USA.

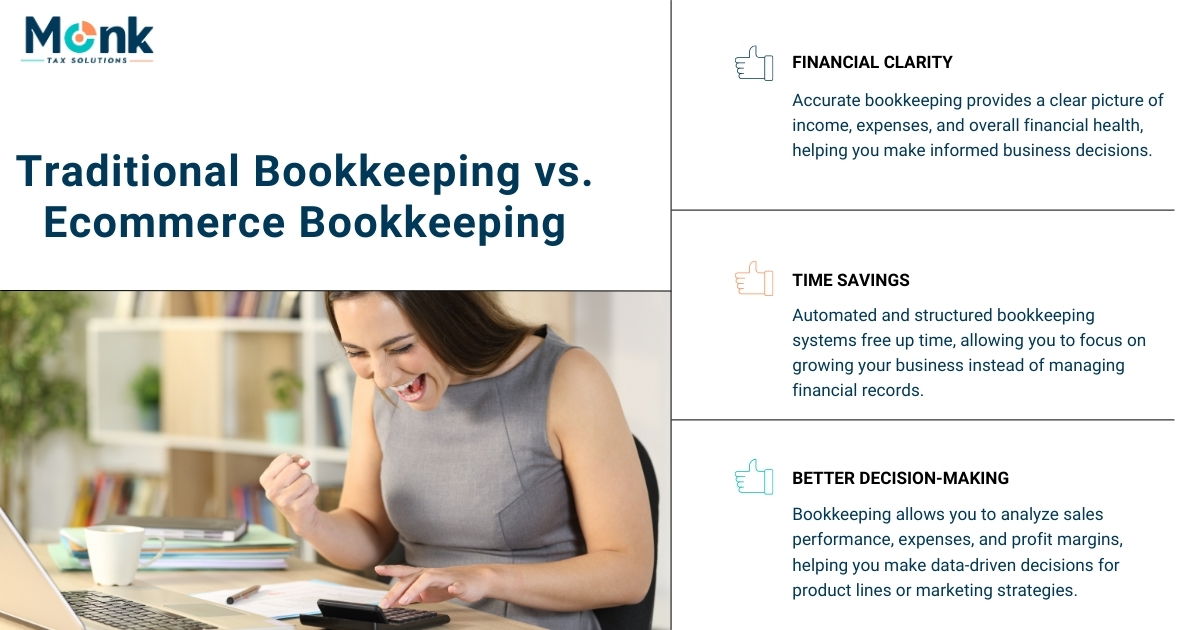

Why Bookkeeping is Crucial for Ecommerce Success

In ecommerce, profit margins can be tight, and a minor oversight in finances can result in major losses. Through bookkeeping, business owners can get a clear picture of their financial health, track revenue and expenses, and monitor their cash flow. Financial insights derived from bookkeeping reveal areas of overspending, high-performing products, and opportunities to improve efficiency.

MonkTaxSolutions provides tailored financial reports that break down revenue, expenses, and profit, offering clear insights that help you make informed decisions about your business’s direction.

Preparing for Tax Obligations

Ecommerce businesses in the USA must comply with various tax regulations, from income tax to sales tax. Bookkeeping is essential for tracking taxable income, eligible deductions, and potential tax credits. Proper record-keeping throughout the year makes tax season much smoother, reducing the risk of errors and potential audits by the IRS. Regular bookkeeping also helps businesses stay up-to-date with changes in tax laws, ensuring compliance. MonkTaxSolutions offers expert tax planning and compliance services, helping businesses reduce tax liabilities and stay compliant.

Key Bookkeeping Basics for Ecommerce Businesses

Income and Expense TrackingIncome and expense tracking is the foundation of bookkeeping. Ecommerce businesses handle revenue from multiple sources — sales, returns, shipping fees, and promotions. Similarly, expenses may include inventory costs, shipping, marketing, and platform fees. Accurately recording each transaction is crucial for calculating profit and loss, setting budgets, and managing cash flow effectively.

MonkTaxSolutions provides an all-in-one solution for income and expense tracking, allowing ecommerce businesses to monitor each financial transaction across various channels and gain a consolidated view of their profitability.

Inventory Management in Bookkeeping

For ecommerce businesses, inventory represents a significant investment and must be accounted for properly. Bookkeeping for ecommerce inventory includes tracking purchases, sales, and any write-offs due to damage or obsolescence. Accurate inventory bookkeeping ensures that the value of assets reflects the real-time state of the business, helping owners make informed decisions about reordering, discounts, and restocking. MonkTaxSolutions can help businesses set up efficient inventory tracking systems, ensuring that they stay on top of inventory costs and valuation.

Setting Up an Effective Bookkeeping System

Choosing the Right Accounting Software

Ecommerce bookkeeping can be complex, with high transaction volumes and a need for detailed reports. Many ecommerce businesses rely on accounting software tailored to online sales, such as QuickBooks, Xero, or FreshBooks. The right software should be able to handle multi-channel transactions, automate data entry, and integrate with ecommerce platforms. Choosing accounting software that aligns with your business needs can save time and reduce errors. MonkTaxSolutions assists businesses in choosing and implementing the best accounting software for their unique needs, helping them integrate their software with popular ecommerce platforms for streamlined operations.

Integrating Ecommerce Platforms with Accounting Tools

Integrating your ecommerce platform (like Shopify, Amazon, or WooCommerce) with accounting software streamlines bookkeeping. This integration automatically imports transaction data, reducing the need for manual entry and lowering the risk of errors. Many accounting tools also support integrations with payment gateways, POS systems, and inventory management software, providing a unified view of finances.

With MonkTaxSolutions’s support, ecommerce businesses can efficiently link their platforms and accounting tools, ensuring real-time data synchronization for accurate and effortless bookkeeping.

Best Practices for Ecommerce Bookkeeping in the USA

Staying Compliant with IRS Regulations

The IRS has strict guidelines for bookkeeping, especially for ecommerce businesses. Maintaining accurate, detailed records of income, expenses, and inventory ensures compliance with tax regulations. This includes adhering to record-keeping standards for deductible expenses, proper categorization of revenue, and managing documents that substantiate expenses (like receipts and invoices).MonkTaxSolutions offers expert guidance in IRS compliance, helping ecommerce businesses avoid penalties and maintain accurate financial records that meet IRS standards.

Setting Up Sales Tax Tracking

Sales tax in the USA can be complex, with regulations varying by state and even by city. Ecommerce businesses must collect and remit sales tax based on the location of the buyer, which can be challenging to track without proper systems. Bookkeeping software that includes sales tax tracking helps ecommerce businesses comply with tax laws by calculating and reporting sales tax accurately.

MonkTaxSolutions provides specialized sales tax tracking solutions that help businesses manage multi-state sales tax obligations, keeping them compliant across all jurisdictions.

Common Challenges in Ecommerce Bookkeeping

Handling Multiple Sales Channels

Ecommerce businesses often sell across multiple platforms, such as their website, Amazon, eBay, and social media. Managing transactions from various channels can be challenging for bookkeeping, as it requires consolidating data, reconciling discrepancies, and accounting for platform fees. A robust bookkeeping system that integrates with all sales channels simplifies the process and ensures accurate reporting. MonkTaxSolutions offers solutions that consolidate sales channel data, helping business owners get a clear view of their finances across multiple platforms.

Managing Returns and Refunds

Returns and refunds are a common occurrence in ecommerce, but they add complexity to bookkeeping. When a product is returned, it affects income, inventory, and potentially sales tax. Proper bookkeeping practices should account for returns in a way that reflects accurate profit margins and inventory levels.

Conclusion

Ecommerce bookkeeping is a vital foundation for success in the online retail world. By staying organized, keeping accurate records, and utilizing tools and expert support like MonkTaxSolutions, ecommerce businesses can achieve greater financial clarity, tax compliance, and operational efficiency. From tracking income and expenses to managing inventory and handling sales tax, proper outsourced bookkeeping helps online businesses thrive in a competitive market. For USA-based ecommerce businesses, meeting IRS standards and managing multi-state sales taxes can be complex, but with the right strategies and professional guidance, these challenges become manageable. Ultimately, a robust bookkeeping system enables ecommerce owners to focus on growth, make data-driven decisions, and build sustainable financial health for the future.